… and a bonus, yay 😄

If this email was forwarded to you, I’d love to see you onboard. You can sign up here:

Firstly, my apologies! Last weeks’ issue was prematurely sent due to my error. I hope you didn’t mind too much. I’ll strive to ensure that it doesn’t happen in the future. I value enormously the privilege I have to communicate with you directly and I would be horrified to learn I over stepped the mark.

Whilst I’m on the subject of apologies, I incorrectly spelt Pohoiki Beach in Issue 23 , but since corrected it on the website.

As a bonus by way of making it up to you, here’s a quick follow-up on the Intel article.

I’ve been thinking of publishing more often, writing a longer issue for the Friday/Weekend and 2 or 3 shorter articles in during the week. Let le know what you think.

Follow-up to Intel’s Pohoiki Beach

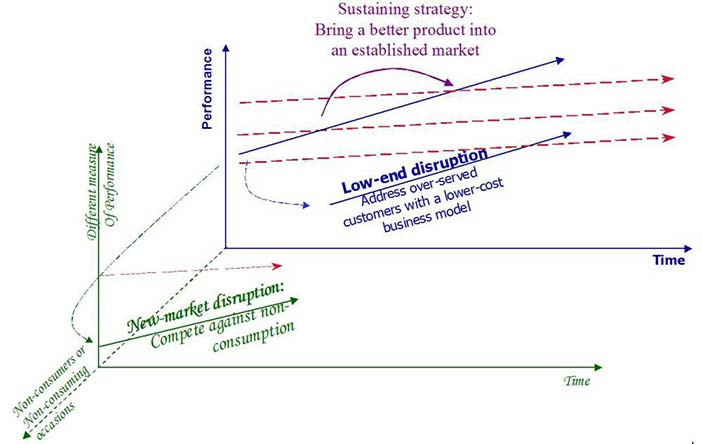

The basic premise of that issue was to introduce disruption theory and how we see it affecting businesses all around us. Disruption theory is a specific set of notions and understandings that allow us to understand when it is happening to us or even predict its eventuality but looking at ourselves from a different perspective. We often throw out the phrase disruption without fully understanding what it really means, so this was my attempt at defining the term.

The other reason for the article was to give a concrete example in the modern world of disruption and how it came to be, my example of Intel pushing further up the quality/price chain as its low-end is being eaten up by the (initially) good-enough products from the various ARM licensees.

This morning I read the blog of a very prominent and very opinionated (but always an excellent read) Apple commentator, Daniel Eran Dilger over at Roughly Drafted. In this article about Apple and Intel, Daniel pretty much confirms, from his point of view the same thing, in that Intel is being disrupted out of the commodity chip business. His argument centres on a few things; Apple’s superiority in chip design, the abstraction of OS and applications from the underlying processor architecture and Intel’s own lack of capacity to innovate the x86 architecture. This is precisely because the commoditisation of the architecture is inevitably driving margins towards zero for Intel.

In disruption theory, we can see that there is a constant fight between integrated and modular systems. New technologies often follow a pattern whereby they provide functionalities that eventually outstrip the pace of the users to fully exploit them. In doing so, the technology providers have to shift strategy from full-throttle innovation, to a strategy of providing just what the customer needs and time it to when its needed. This shift creates a different mindset in the technology provider, forcing them to extract more and more value from the value chain, eventually modularising what was once proprietary and integrated. This inevitably opens the door to disruption by the “just good enough” competitors to start eating away at market share.

However, there is at times, a shift in customer expectations that resets the capacity of the final users to utilise a new technology, that forces the technology providers to embark upon break neck innovation, the cycle restarts!

Source: The Innovator’s Solution, Clayton Christensen

Apple buying Intel’s modem chip business is potentially one such scenario. Remember Apple recently settled with Qualcomm over disputed contract details regarding the supply of modems for Apple’s iPhones and iPads. Apple tried to reduce its exposure to the, very stiff, Qualcomm contracts by dual-sourcing Intel and Qualcomm modems, but that subsequently back-fired with Qualcomm cutting Apple’s supply completely off in 2018. Apple eventually settled out of court and then went on to buy Intel’s model business for 1B USD, announced on the 25th of July.

I’m guessing Apple has seen the possibility in owning the model business to reset the disruption cycle and extract great value from owning the design for its proprietary hardware, namely all of its own iOS devices. This neatly falls in place with the debut of much faster cellular services (read 5G) being deployed (slowly) around the world. Perhaps Apple has some interesting plans in how cellular services can be further integrated in to its hardware driving even further differentiation in a market where commodity wins — if we’re talking about shipping numbers.

Apple doesn’t play the game of selling the most units. Apple plays the game of selling something fully-baked at very high margins. Apple’s gross-margin in the latest quarter’s result … between 37.5 and 38.5 percent. Yes, you read that! To put that in perspective, utilities companies typically have 9%, energy suppliers 14%. Only tobacco provides margin in excess of 20-odd percent.

Reading List

One bonus article to read too … My, my! I’m spoiling you this week 😉

Apple joins Google, Facebook, and Microsoft in data-sharing project

With data becoming central to business use, central to B2C use, it’s only inevitable that some form of universal governance of data will happen. The GDPR goes some way towards that, but it doesn’t address extremely difficult technical issues, only preferring to penalise businesses of sloppy data usage. The Data Transfer Project hopes to help in this regard. My only frustration is that Facebook is included given their track-record of bad data handling (to say the least), but I suppose it’s better to have the bad actors included, rather than separated where they could do much more damage.

The Future is Digital Newsletter is intended for anyone interesting in learning about Digital Transformation and how it affects their business. I strongly encourage you to forward it to people you feel may be interested.

Remember, you can read all the free back issues here:

Thanks for being a supporter, have a great day.